Executive Summary

The Consumer Financial Protection Bureau (CFPB) was established in 2010 in the wake of the worst financial crisis in decades. Its mission is to identify dangerous and unfair financial practices, to educate consumers about these practices, and to regulate the financial institutions that perpetuate them.

To help accomplish these goals, the CFPB has created and made available to the public the Consumer Complaint Database. The database tracks complaints made by consumers to the CFPB and how they are resolved. The Consumer Complaint Database enables the CFPB to identify financial practices that threaten to harm consumers, and it enables the public to evaluate both the performance of the financial industry and of the CFPB.

This is the fifth in a series of reports that review complaints to the CFPB nationally and on a state-by-state level. In this report we explore consumer complaints about debt collection, with the aim of uncovering patterns in the problems consumers are experiencing with debt collectors and documenting the role of the CFPB in helping consumers successfully resolve their complaints.

Consumer complaints about debt collection are common. Between July 2013 – when the Consumer Financial Protection Bureau began recording data on debt collection – and January 16, 2014, the CFPB recorded more than 11,000 complaints about debt collection – the second-highest volume of complaints received about any financial service during that time period.

- Consumers have filed an average of about 2,000 complaints per month with the CFPB about debt collection.

- Despite being the newest type of consumer complaint accepted by the CFPB, complaints about debt collection practices now rank second only to complaints about mortgages in average monthly complaint volume.

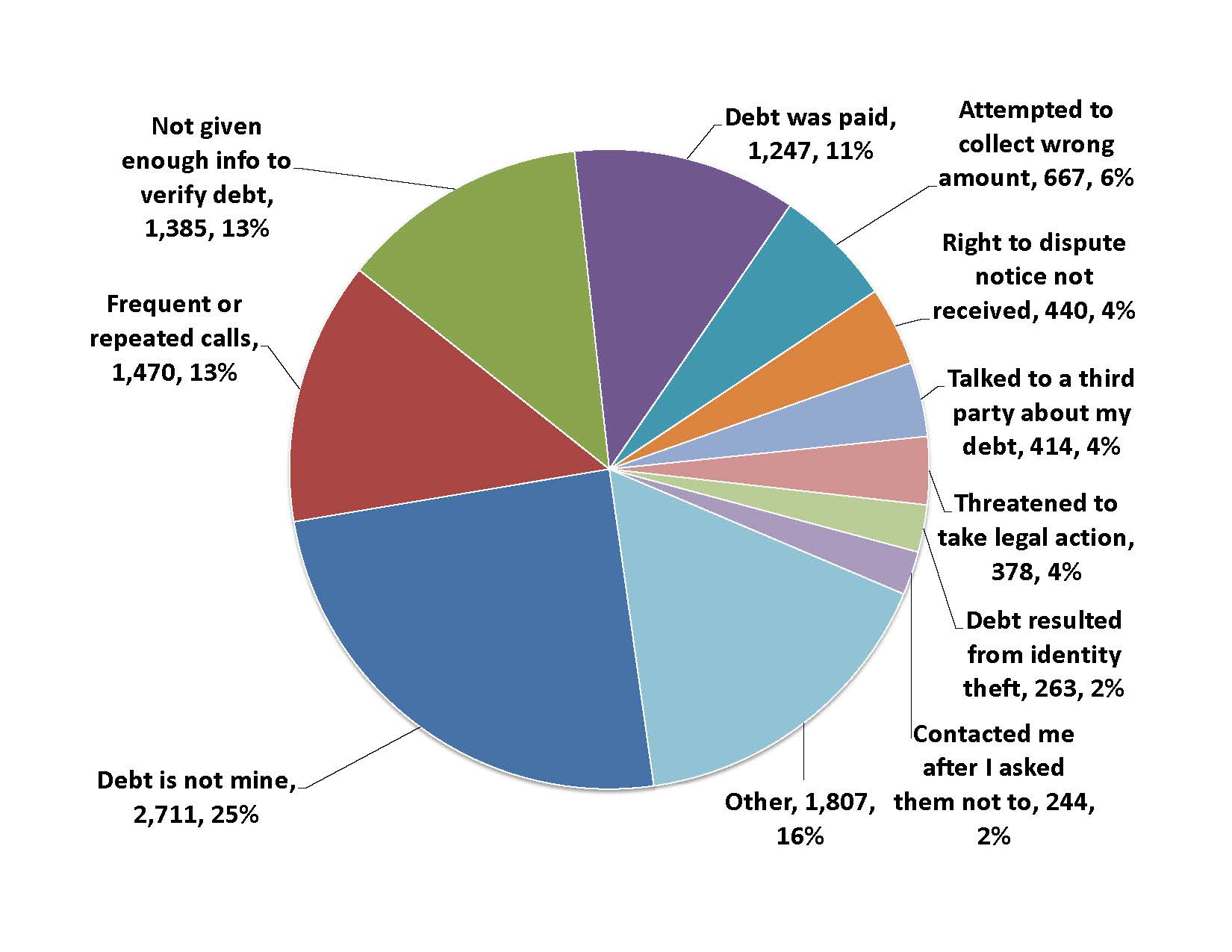

Consumers face a wide array of problems with debt collection.

- More than 2,700 consumers complained about debt collectors’ attempts to collect debt that did not belong to the consumers, making it the most common cause of complaints to the CFPB.

- Other top causes for complaint included: frequent or repeated debt collection calls; not being given enough information about the debts owed; and attempted collection of debts that had already been paid.

Figure ES-1. Top Causes of Complaints to the CFPB about Debt Collection

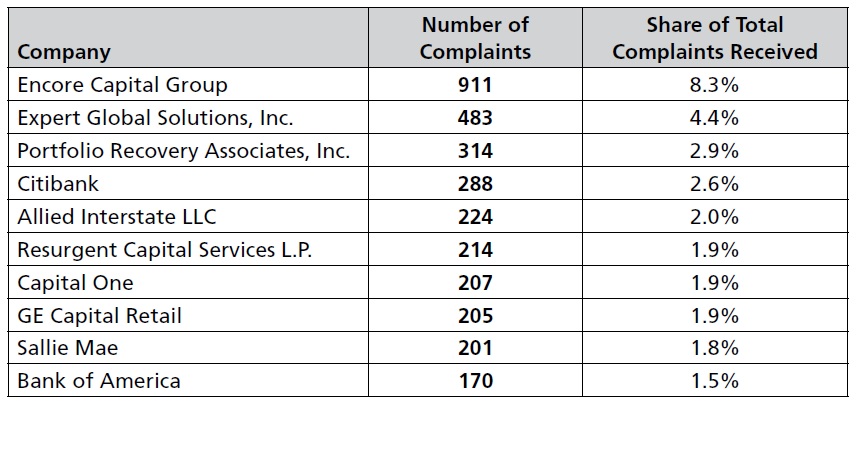

The list of top complaint recipients includes both original creditors and third-party debt collection agencies.

- Encore Capital Group, a third-party company that buys debts from banks and other financial institutions and attempts to collect on them—and is the parent of debt collection firm Midland Credit Management and other subsidiaries—was the most complained-about company by total number of complaints. It was followed by Expert Global Solutions, Portfolio Recovery Associates, Inc. and Citibank.

Table ES-1. Top Ten Companies by Complaints to the CFPB about Debt Collection

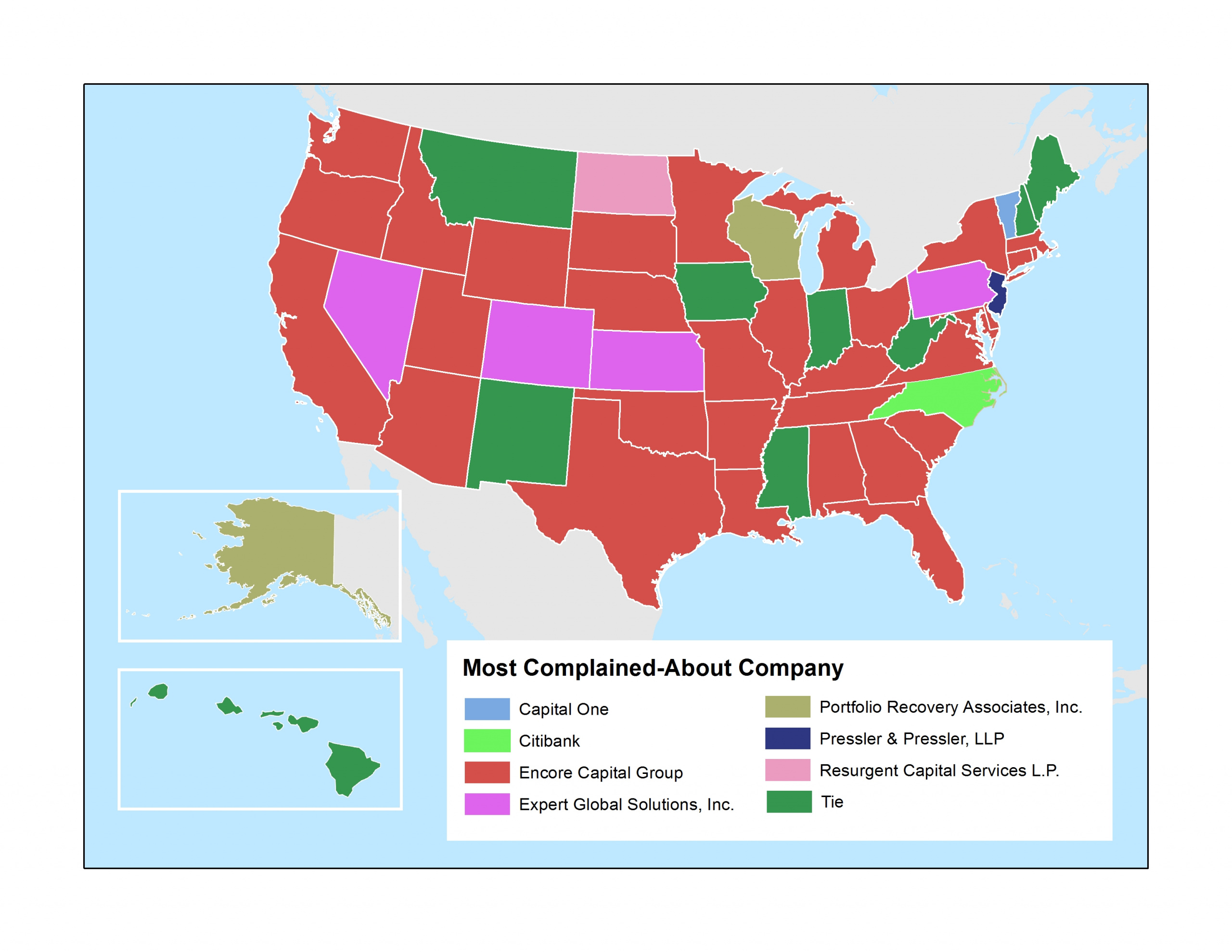

Complaints about companies vary by state, and state residents vary in their tendency to reach out to the CFPB.

- San Diego-based Encore Capital Group was the most complained-about company in 31 states. In five states, Expert Global Solutions, Inc. was the most complained-about company. Debt buyer Portfolio Recovery Associates, Inc. was the most complained-about company in Alaska and Wisconsin, while Citibank was the most complained-about company in North Carolina. Law firm Pressler and Pressler, LLP received the most complaints in New Jersey. (See Figure ES-2.)

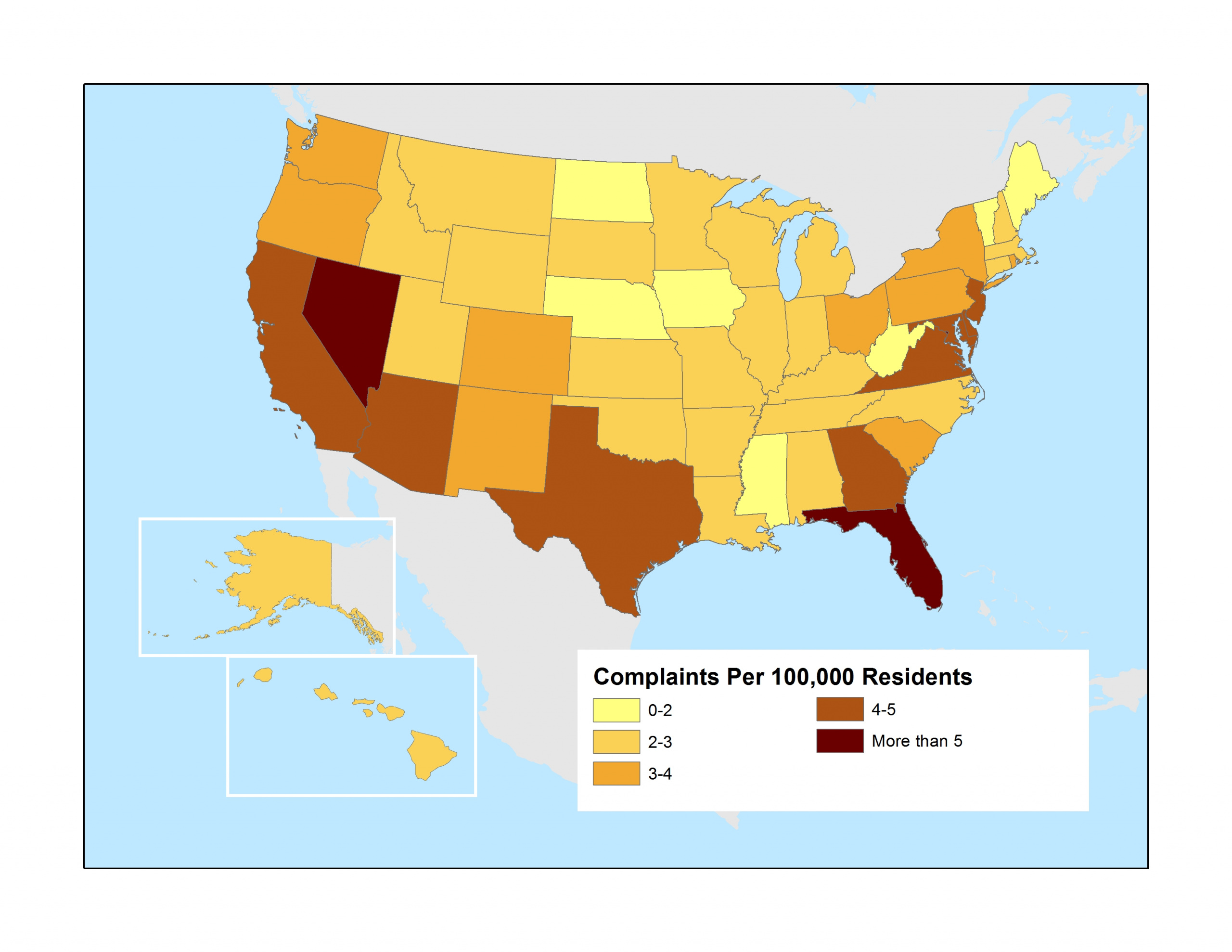

- The District of Columbia had the most complaints per capita, followed (in order) by Nevada, Florida, Delaware, Maryland, Georgia, Virginia, New Jersey, Arizona and Texas. (See Figure ES-3.)

Figure ES-2. Encore Capital Group Is the Most Complained-About Company in 31 States

Figure ES-3. Complaints About Debt Collection Vary by State

The CFPB is making a significant difference for consumers facing difficulties with debt collectors.

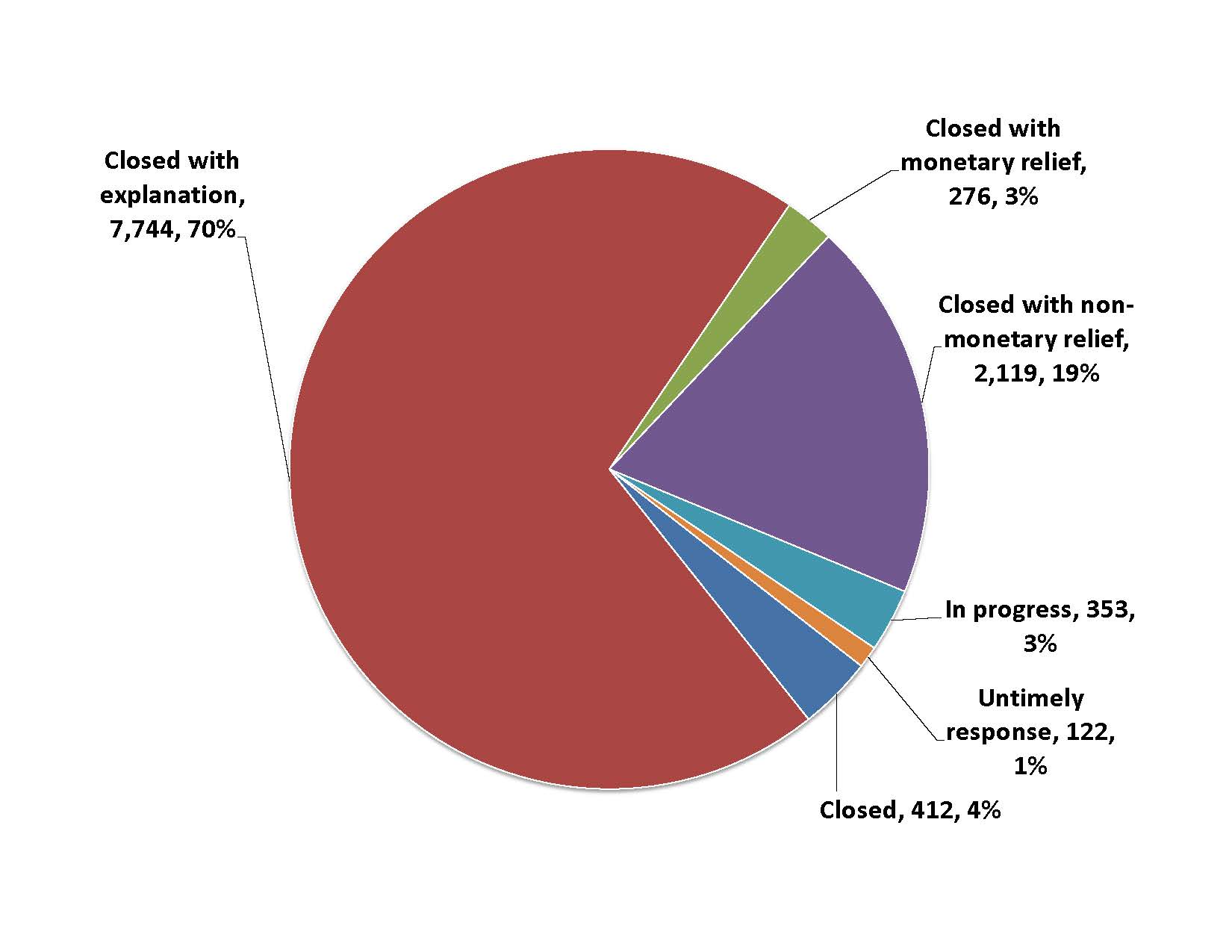

- The CFPB has helped more than 2,300 consumers – or more than one in five complainants – to receive monetary or non-monetary relief as a result of their debt collection complaints. (See Figure ES-4.)

Figure ES-4. 22 Percent of Consumers Received Relief after Complaining to the CFPB

- Companies vary greatly in the extent to which they respond to consumer complaints with offers of monetary or non-monetary relief. Four of the 20 most complained-about companies – Convergent Outsourcing, Dynamic Recovery Solutions, Inc., Diversified Consultants, Inc., and I.C. System, Inc. – reported providing no relief, either monetary or non-monetary, to any of the consumers who complained to the CFPB. Allied Interstate LLC and Portfolio Recovery Associates, Inc. were the most likely to report extending monetary or non-monetary relief, providing relief for 98 percent and 79 percent of complaints, respectively.

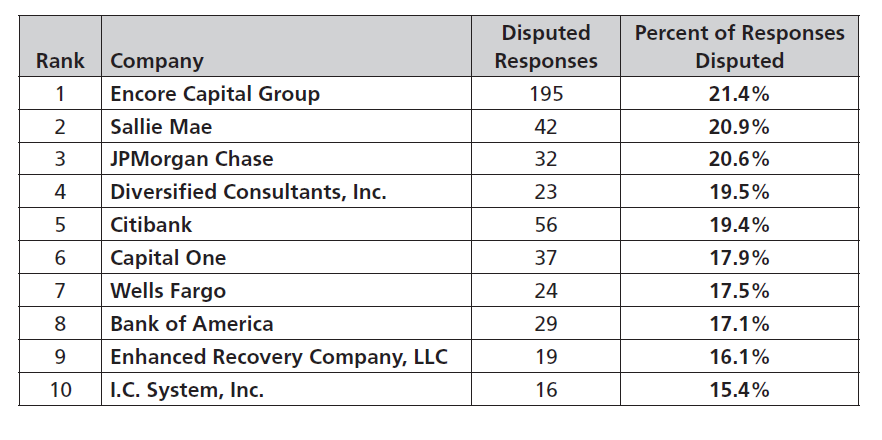

- About 16 percent of responses from debt collectors were deemed unsatisfactory by consumers and were subjected to further dispute.

- Of the 20 companies with the most overall complaints, the company with the greatest proportion of disputed responses was Encore Capital Group, with 21.4 percent of responses disputed. Of these same companies, Expert Global Solutions had the lowest proportion of disputed responses, with 5.2 percent of responses disputed.

Table ES-2. Companies with the Highest Dispute-to-Complaint Ratios[1]

The Consumer Financial Protection Bureau’s Consumer Complaint Database is a key resource for consumer protection. To enhance the ability of the CFPB to respond to consumer complaints, the CFPB should:

- Add more detailed information to the database, such as actual complaint narratives, detailed complaint categories and subcategories, complaint resolution details, consumer dispute details, and data regarding membership in classes protected from discrimination by law. Expanded complaint-level details should also include more information about amounts and types of monetary and non-monetary relief. The CFPB should also …” to “Software and other techniques should be used to protect consumer privacy by giving consumers the right not to provide details and by taking steps to prevent the release of personally identifiable information or the re-identification of consumers. It is critical that the CFPB achieve the disclosure of more individual complaint details while simultaneously making every reasonable effort to protect personal data.

- Add a field listing company subsidiaries, which are often the firms with which consumers actually interact. For example, Encore Capital Group, the company with the greatest number of debt collection complaints in the CFPB database, does business under the names of several subsidiaries. Adding subsidiary company information will enable consumers to better apply the information in the CFPB database to their own experiences, and to the choices they make in the marketplace.

- Provide regular trend analyses and monthly detailed reports on complaint resolutions and disputes.

- Simplify the interfaces that allow users to summarize complaint database reports in graphical and printable formats.

- Publicize information about the CFPB complaints process in forums that are likely to be seen by consumers. The agency should develop more outreach mechanisms for consumer education about the database and its services for consumers, including creating educational materials to be distributed on- and off-line, holding more educational events outside Washington, D.C., and partnering with non-profit organizations.

- Develop free applications (apps) for consumers to download to smartphones to access information about how to complain about a firm and how to review complaints in the database.

- Expand the Consumer Complaint Database to include discrete complaint categories for high-cost credit products such as auto title loans and prepaid cards. We commend the CFPB for adding payday loan complaints to the database in November 2013.

- Continue to use the information gathered from the Consumer Complaint Database, from supervisory and examination findings, and from other sources to require a high, uniform level of consumer protection and ensure that responsible industry players can better compete with those who are using harmful practices.

To protect consumers from unfair debt collection practices, the agency should:

- Stop debt collectors and buyers from collecting debts without proper information and documentation about the debt or records of prior communications with the consumer.

- Stop debt collectors from bringing robo-signed cases in court.

- Crack down hard on widespread use of threats, harassment and embarrassment and make it easier for consumers to demand a stop to unwanted communications.

- Prevent debt collectors from making robo-calls to cell phones, sending email or leaving messages in places where they might be seen or heard by others.

- Require debt collectors to verify that they are collecting the correct debts from the correct consumers before they start collections.

- Clarify that debt collection law gives consumers the right to sue to stop unfair practices and to collect multiple penalties for multiple violations.

- Protect servicemembers by strictly limiting contact with their commanders to verifications of employment and address.

- Protect all consumers by mandating additional disclosures concerning the effect of paying debts on their credit reports, such as a disclosure that says, “Paying this debt will not remove it from your credit report.”

- Adopt additional reforms advocated by the National Consumer Law Center, Americans for Financial Reform, U.S. PIRG and other organizations.

[1] Only top 20 companies by total number of complaints analyzed. Of these 20, top ten companies by percent disputed are shown.